Global Wireless Infrastructure Market by Type, Infrastructure, Application, Region – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

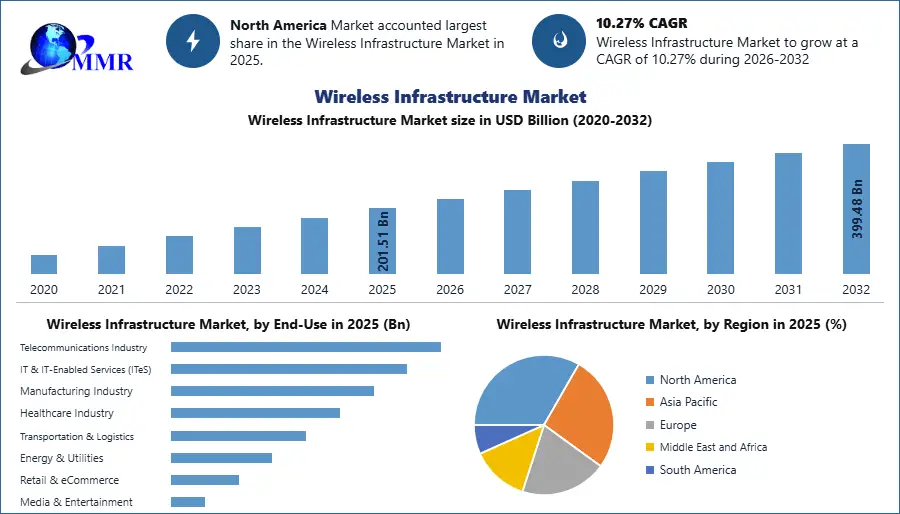

Global Wireless Infrastructure Market size was valued at USD 201.51 Bn in 2025 and is expected to reach USD 399.48 Bn by 2032, at a CAGR of 10.27%.

Overview

Wireless infrastructure refers to the hardware and software resources that facilitate wireless communication, including cell towers, small cells, Wi-Fi hotspots, routers, and backhaul systems. Its primary use is to support mobile communication and internet access, enabling seamless connectivity for devices such as smartphones, tablets, and IoT devices. Applications include mobile broadband, public safety communications, smart city initiatives, and industrial automation. Market growth is driven by increasing mobile data traffic, the expansion of 5G networks, rising demand for high-speed internet, and advancements in IoT technologies. The need for improved network capacity and coverage, alongside evolving consumer expectations for reliable and fast connectivity, further propels the wireless infrastructure market. The term wireless network infrastructure is used commonly concerning mobile core and macrocell RAN network infrastructure. The popularity of 4G, LTE, 5G based high-speed data connectivity and performance across the globe is one of the key drivers in the global Wireless Infrastructure Industry.

Governments provide various incentives to promote wireless infrastructure development. Financial incentives include grants, subsidies, tax credits, and low-interest loans. Regulatory incentives involve streamlined permitting, spectrum allocation, and supportive zoning policies. Policy initiatives encompass universal service funds, public-private partnerships, and digital inclusion programs. Additionally, governments support research and development in wireless technologies through funding and public research institutions. Infrastructure sharing is also encouraged to reduce costs. Examples include the FCC's Rural Digital Opportunity Fund in the U.S., the EU's Connecting Europe Facility, and India's BharatNet project. These measures aim to enhance connectivity, bridge the digital divide, and foster economic growth and innovation. Also, rapid urbanization, industrialization, technological advancements and enterprise mobility are some of the powerful factors behind the evolution of the global wireless infrastructure Market.

To know about the Research Methodology:-Request Free Sample Report

To know about the Research Methodology:-Request Free Sample Report

Wireless Infrastructure Market Dynamics

Proliferation of 5G Technology to Drive the Market Growth

The wireless infrastructure market is experiencing significant growth due to the rapid deployment of 5G technology. This next-generation wireless network promises unprecedented speed, low latency, and enhanced connectivity, catering to the increasing demand for high-speed data transmission. As consumers and industries alike embrace smart devices, the Internet of Things (IoT), and advanced applications such as augmented reality (AR) and virtual reality (VR), the need for robust and expansive wireless infrastructure becomes paramount.

Telecommunications companies are investing heavily in 5G infrastructure, including small cells, macro cells, and distributed antenna systems, to ensure comprehensive coverage and capacity. In 2023, global 5G connections surged to 1.76 billion, marking a 66% year-over-year increase with 700 million new connections. North America led with 29% of all wireless connections being 5G, growing by 64% and adding 77 million new connections, totaling 197 million. By year-end, South America also saw significant progress with 582 million 4G LTE connections and 39 million 5G connections. Omdia forecasts global 5G connections to reach 7.9 billion by 2028, with North America hitting 700 million. 5G data traffic is expected to dominate, making up 76% of all technology data traffic by 2028. There are 314 commercial 5G networks worldwide, projected to grow to 450 by 2025. India’s country-wide 5G Availability increased throughout 2023. 5G Availability improved from 28.1% in Q1 to 52.0% in Q4 2023, representing a 23.9 percentage point increase within a year. Reliance Jio’s 5G availability rate during Q4 2023 was 68.8%, 38.5 percentage points higher than Airtel’s 30.4%. Also, government initiatives and regulatory frameworks supporting the rollout of 5G networks further propel market growth. This technological evolution enhances user experiences and drives innovation across sectors such as healthcare, automotive, and manufacturing, positioning 5G as a critical catalyst for the wireless infrastructure market growth.

5G share of total mobile connections in 2025-2032 by Region(%)

The 5G share of total mobile connections is projected to grow significantly by 2032, driving the wireless infrastructure market. This growth is fueled by increasing demand for high-speed internet, IoT advancements, and the expansion of smart cities. Key regions like North America, Europe, and Asia-Pacific have substantial increases in 5G adoption, necessitating upgraded infrastructure. Investment in network densification, small cells, and fiber backhaul is crucial. Additionally, government initiatives and competitive pressures among telecom operators accelerate infrastructure deployment, enhancing connectivity and supporting emerging technologies such as autonomous vehicles and augmented reality.

Rising Demand for Mobile Data to Boost the Market

The exponential increase in mobile data consumption is a crucial driver of growth in the wireless infrastructure market. With the surge in smartphone usage, streaming services, social media, and cloud-based applications, consumers and businesses require faster and more reliable wireless connectivity. This demand pressures telecom operators to upgrade their network infrastructure to accommodate higher data traffic volumes and improve service quality.

The shift towards remote work and digital transformation initiatives across various industries further amplifies the need for robust wireless networks. Investments in network densification, spectrum acquisition, and advanced technologies such as Massive MIMO and beamforming are essential to meet these growing demands and boost the Wireless Infrastructure Market growth. As operators strive to enhance network performance and user experience, the continuous expansion and modernization of wireless infrastructure become imperative. This trend not only boosts market growth but also fosters innovation in network solutions and services, ensuring seamless connectivity in an increasingly digital world.

Edge Computing Integration Enhances Wireless Infrastructure Value and Creates Lucrative Opportunity for Market Growth

Edge computing is a distributed computing architecture framework that brings computer processing from a distant data center closer to the source of data generation and consumption. The reason for doing this is to reduce latency by moving away from completely centralized operations. This can enable innovations and services while improving the end-user experience. Edge coupled with 5G's higher connectivity speeds, for example, supports advanced robotics, artificial intelligence (AI) and autonomous technology, massive Internet of Things (IoT) and augmented and assisted reality (AR). The combination of 5G and edge computing has the potential to be a catalyst for innovation across numerous industries and drive the Wireless Infrastructure Market. In particular, the growing trend of processing and storing data closer to the edge of the network and away from centralized data centers have a huge impact on the future of telecommunications. Telecom edge computing offers operators a strategic opportunity to enhance operations and leverage their technology expertise to generate more revenue and move further up the value chain.

As data processing moves closer to the source of data generation, reducing latency and bandwidth usage becomes crucial. Edge computing enables real-time data analysis and decision-making at the network edge, which is essential for applications such as autonomous vehicles, industrial automation, and augmented reality. Edge computing integration presents a transformative opportunity for the wireless infrastructure market. To support this shift, wireless infrastructure must evolve to include edge data centers and enhanced connectivity solutions. Telecom operators and infrastructure providers leverage this trend by developing edge-ready infrastructure that handle the increased data processing demands. This includes investing in edge nodes, micro data centers, and advanced wireless technologies including 5G and Wi-Fi 6. By integrating edge computing capabilities, the wireless infrastructure industry offer more efficient and responsive networks, driving new business models and revenue streams while meeting the growing needs of data-intensive applications and services.

Key Factors Influencing Investments in Wireless Infrastructure and Restrain the Market Growth

The growth of the wireless infrastructure market is restrained by several factors including regulatory red tape, which delay project approvals and increase costs. Workforce shortages, particularly in skilled labor for 5G network buildouts, hinder timely deployment. Limited spectrum availability and high auction costs constrain network expansion. Additionally, the complexities of coordinating with various stakeholders, such as local governments and utility companies, can slow progress and increase operational challenges.

Wireless Infrastructure Market Segment Analysis

By Type:

Based on type, the 4G segment held the largest Wireless Infrastructure Market share in 2025. The growing implementation of 5G, 4G networks continues to be the backbone of mobile communication infrastructure in many regions. They provide high-speed mobile internet services where 5G deployment is still in progress or coverage is limited. 4G networks offer widespread coverage in urban, suburban, and rural areas, ensuring reliable connectivity and fast data services for a broad user base. Wireless operators are investing in expanding and upgrading their 4G networks to ensure seamless coverage and capacity. The steady growth of the 4G segment is supported by the availability and affordability of 4G-compatible devices, such as smartphones, tablets, and IoT devices.

By Application:

The commercial segment is projected to dominate the Wireless Infrastructure Market share from 2025 to 2032. Companies are adopting digital transformation programs to enhance customer satisfaction, boost productivity, and create new business opportunities. Wireless infrastructure is crucial for supporting digital transformation, offering high-speed connectivity, mobility, and access to cloud-based applications and services. The retail and hospitality sectors are investing in wireless infrastructure to improve client interaction, optimize operational efficiency, and deliver personalized experiences. Wireless connectivity is vital for the seamless operation of digital signage systems, Wi-Fi networks, location-based services, and mobile payment options. In healthcare, wireless infrastructure is being adopted to enable telemedicine, remote patient monitoring, electronic health records (EHR), and medical IoT devices.

Wireless Infrastructure Market Regional Analysis

North America dominated the largest global wireless infrastructure market share in 2025. This growth is driven by the increased penetration of LTE and 4G services in developed countries like the U.S. and Canada. The adoption of wireless devices is measured at nearly about 95% in the enterprise market in the U.S.A. The Healthcare sector toward high-speed communications for video streaming surgeries is expected to drive the growth in the wireless infrastructure market. In-building wireless networks are essential for providing cellular coverage in various large buildings, including stadiums, hospitals, and airports. These networks, which have evolved from supporting 3G to 5G, complement Wi-Fi by handling larger capacities and offering better security. No single solution fits all enterprises, as needs vary by type and size of the building. Options range from neutral-host distributed antenna systems (DAS) to operator-owned small-cell architectures. In 2022-23, the U.S. spent $567 million on building and operating these networks, excluding Wi-Fi. This included $274 million on construction and $293 million on operations, with 747,400 indoor small-cell nodes in use. Despite COVID-19 impacts, the commercial IBW market outlook remains positive as in-building connectivity needs grow.

Asia Pacific region is projected to be a leading region in the global wireless infrastructure market. The developing country India holds the largest Business Process Outsourcing (BPO) market, which requires significant wireless infrastructure. Additionally, the growing number of mobile internet users in Asia has contributed to the rise in the demand for wireless communication networks. Trends like Bring-Your-Own-Device (BYOD) and Wear-Your-Own-Device (WYOD are expected to increase the demand for wireless infrastructure. The BYOD/WYOD empowers employees to bring/wear their personal devices to work and use them to access enterprise data. The growing global economy and expansions into multiple markets have encouraged enterprises to grow rapidly. For handling larger volumes of data every day, enterprises are moving toward high-speed data solutions, which empower them to share data across numerous verticals and countries quickly. Additionally, an increase in enterprise mobility, assisting employees to work from anywhere using wireless devices and platforms of their choice has expected an increased need for wireless communication.

Wireless Infrastructure Market Recent Industry Developments (2025–2026)

| Date | Company | Development | Impact |

|---|---|---|---|

| 12 February 2026 | Huawei Technologies Co., Ltd. | Launched the IntelligentRAN platform featuring Level 4 automation for managing over 1 million cell sites globally. | Reduces operational complexity and achieves up to 95% energy reduction in low-traffic scenarios using Extreme Deep Sleep technology. |

| 27 January 2026 | Nokia Corporation | Unveiled the Habrok radios powered by ReefShark System-on-Chip (SoC) technology for mid-band 5G deployments. | Enables high-capacity coverage with up to 800 MHz In-Building Wireless (IBW) capacity for fragmented spectrum management. |

| 14 January 2026 | T-Mobile US, Inc. | Successfully completed the acquisition of UScellular's wireless operations and spectrum assets. | Consolidates the U.S. market into a three-carrier model, driving intensified investment in nationwide 5G infrastructure and network density. |

| 05 November 2025 | Telefonaktiebolaget LM Ericsson | Introduced a suite of seven 5G Advanced software products to enhance network programmability. | Allows operators to deploy AI-driven performance optimizations across 11 million cells daily through cognitive software. |

| 18 September 2025 | SpaceX | Signed a $19 billion agreement to acquire Echostar's AWS-3 and AWS-4 spectrum licenses. | Facilitates the global expansion of Starlink's Direct-to-Cell services, integrating satellite and terrestrial wireless infrastructure. |

| 10 June 2025 | Cisco Systems, Inc. | Released the AI Canvas assistant integrated with a networking-specific Large Language Model (LLM) for infrastructure management. | Provides agent-driven automation for Private 5G and cloud-native platforms, improving deployment speed for enterprise networks. |

Wireless Infrastructure Market Scope: Inquire before buying

| Wireless Infrastructure Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 201.51 USD Billion |

| Forecast Period 2026-2032 CAGR: | 10.27% | Market Size in 2032: | 399.48 USD Billion |

| Segments Covered: | by Type | 2G/3G (Legacy Networks) 4G LTE 5G |

|

| by Infrastructure | Macro Cells Small Cells Radio Access Network (RAN) Distributed Antenna System (DAS) Mobile Core Network Backhaul (Microwave/Fiber) Others |

||

| by Application | Telecom Operators Enterprises Government & Public Safety Defense & Military Industrial Commercial |

||

| by End-Use | Telecommunications Industry IT & IT-Enabled Services (ITeS) Manufacturing Industry Healthcare Industry Transportation & Logistics Energy & Utilities Retail & eCommerce Media & Entertainment |

||

Wireless Infrastructure Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, ASEAN, and Rest of APAC)

South America (Brazil, Argentina Rest of South America)

Middle East & Africa (South Africa, GCC, and Rest of ME&A)

Wireless Infrastructure Key Players

- Qualcomm Technologies Inc.

- Huawei Technologies Co.Ltd.

- Telefonaktiebolaget LM Ericsson

- Nokia Corporation

- Samsung Electronics Co. Ltd.

- ZTE Corporation

- Cisco Systems Inc.

- NEC Corporation

- Fujitsu (Tokyo Japan)

- Ciena Corporation

- Juniper Networks Inc.

- Capgemini Engineering

- NXP Semiconductors N.V.

- ADTRAN Inc.

- Motorola Solutions Inc.

- CommScope Holding Company Inc.

- Huber+Suhner AG

- Mavenir Systems Inc.

- Parallel Wireless Inc.

- Airspan Networks Holdings Inc.

- Corning Incorporated

- Vertical Bridge Holdings LLC

- DigitalBridge Group Inc.

- American Tower Corporation

- Crown Castle Inc.